The inflation woes don’t just end for Malaysians at the food and necessities paying counter. Added to that is the housing woes that are plaguing many of the cities, especially for Penang, Johor Bahru and the Klang Valley. Specifically, burgeoning house prices and shortage of affordable housing in the major urban centres have now left many working families living in cramped housing conditions with their retired or aged parents.

The inflation woes don’t just end for Malaysians at the food and necessities paying counter. Added to that is the housing woes that are plaguing many of the cities, especially for Penang, Johor Bahru and the Klang Valley. Specifically, burgeoning house prices and shortage of affordable housing in the major urban centres have now left many working families living in cramped housing conditions with their retired or aged parents.

According to the National Property Centre (NAPIC), average house prices in Malaysia have risen by 40 percent since 2000, yet in the same period the average wage earner has only saw his pay increased by a measly 2.6 percent. The increase in house prices are more staggering in Penang, Kuala Lumpur, Selangor and Johor. For 2010 alone, the house prices in these states saw an average increase of 22 percent (Malaysiakini, 12 May 2011).

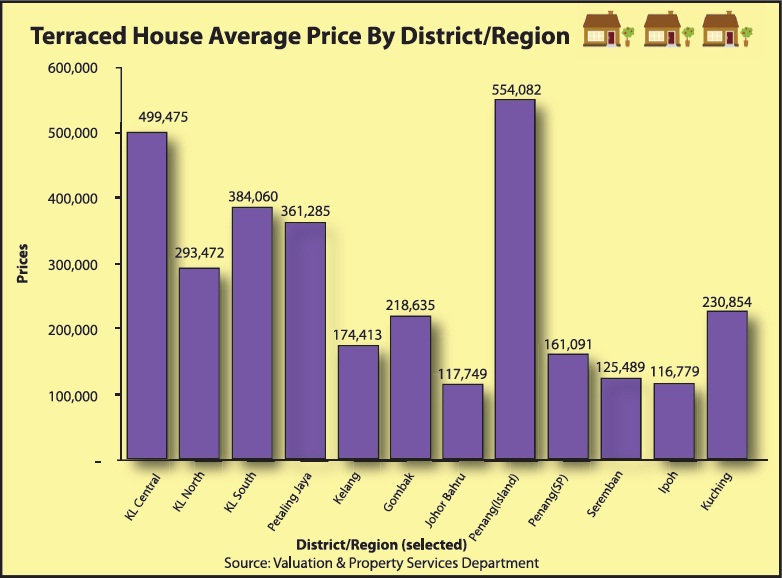

Anecdotal evidence suggests that even a single professional earning above RM 3,000 would struggle to be able to find affordable abodes. Average terrace house prices in Kuala Lumpur have increased by RM 40,000 in 2010 alone (Malaysian House Price Index Data Jan –Mar 2011, Valuation and Property Services Department).

Yet in the midst of all this is the irony of plenty in midst of poverty; NAPIC reported that there are around 67,000 luxury condominium units unsold as at December 2010. How did we reach such a predicament?

The National House Buyers Association (HBA) recently made an announcement that house price increases have reached astronomical level. HBA has blamed it on unsustainable speculation fuelled by easy credit and low interest rates. Added to the “unholy alliance of certain developers, valuers and banks”, the government’s ill-informed policies have also contributed to the mire. (The Malaysian Insider, 4 May 2011)

To begin with, anyone looking to purchase his third, fourth and fifth houses is still entitled to get loan financing from the banks with the corresponding margin of financing at 70 percent, 60 percent and 50 percent respectively. Ease of credit is easy ammunition for speculators to flip properties. HBA has called on Bank Negara (BNM) to reduce the margin of financing available for this class of purchasers.

In addition, change in taxation policies has fuelled the boom in speculating activities. Before 2010, Malaysia practiced a scaling rate of 30 percent in the first year of purchase, 20 percent in the second year, 15 percent in the third year, 5 percent in the fourth year and nil for fifth and subsequent years.

In addition, change in taxation policies has fuelled the boom in speculating activities. Before 2010, Malaysia practiced a scaling rate of 30 percent in the first year of purchase, 20 percent in the second year, 15 percent in the third year, 5 percent in the fourth year and nil for fifth and subsequent years.

The previous scaling rate was effective in clamping down on property speculation. However in 2010, the government revise the Real Property Gains Tax (RPGT) rate to 5 percent for the disposal of houses in the first to fifth year of purchase and 0 percent on the sixth year onwards.

The reduction in RPGT rates encourages more property transactions, contributing to the cash-strapped government’s coffers. But at what cost to the people? In effect, it is giving a discount of 25 percent (for first year disposals) to speculators to flip properties. Will we see an entire generation of homeless dwellers as a result of the government’s greed and folly? -The Rocket